Business

Govt drive returns Rs 2,000 crore unclaimed savings to rightful owners

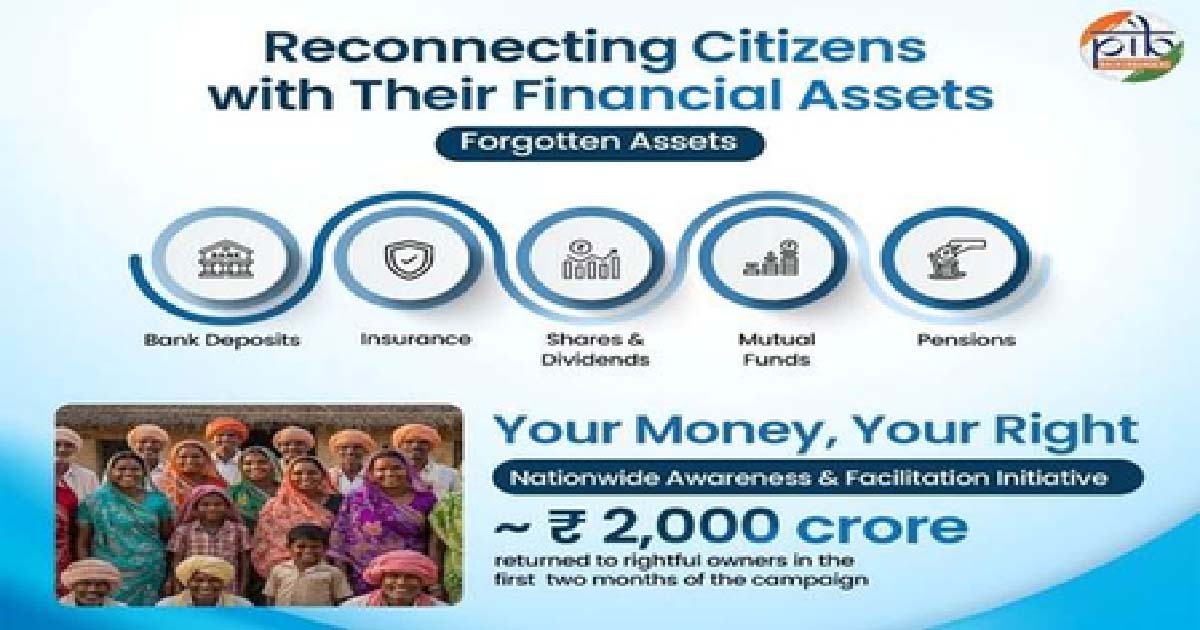

New Delhi, Dec 26: The government has succeeded in returning to the rightful owners a total amount of nearly Rs 2,000 crore that was stuck as “unclaimed savings” across banks, insurance, mutual funds, dividends, shares, and retirement benefits held within the regulated financial system, according to an official statement issued on Friday.

The funds have been restored through the Centre’s “Your Money, Your Right” nationwide awareness and facilitation initiative, launched in October 2025 to help citizens identify and reclaim unclaimed financial assets. The initiative is being coordinated by the Finance Ministry’s Department of Financial Services, with financial sector regulators reaching across digital portals with district-level facilitation.

Across generations, Indian families have saved carefully through opening bank accounts, purchasing insurance policies, investing in mutual funds, earning dividends from shares, and setting aside money for retirement. These financial decisions are taken with a hope and responsibility, often to secure children’s education, support healthcare needs, and ensure dignity in old age.

Yet, over time, a significant portion of these hard-earned savings has remained unclaimed. The money has not vanished, nor has it been misused. It lies safely with regulated financial institutions, separated from its rightful owners due to a lack of awareness, outdated records, changes in residence, or missing documentation. In many cases, families are simply unaware that such assets exist.

The volume of unclaimed financial assets in India is significant and spans multiple segments of the formal financial system. Indicative estimates suggest that Indian banks together hold around Rs 78,000 crore in unclaimed deposits. Unclaimed insurance policy proceeds are estimated at nearly Rs 14,000 crore, while unclaimed amounts in mutual funds are about Rs 3,000 crore. In addition, unclaimed dividends account for around Rs 9,000 crore, according to official figures.

Together, these amounts underline the scale of unclaimed savings belonging to citizens that continue to remain unused, despite being securely held within the financial system.

Your Money, Your Right is a nationwide effort to reconnect citizens with these forgotten financial assets and ensure that money that belongs to individuals and families ultimately finds its way back to them.

These unclaimed financial assets arise when money held with financial institutions is not claimed by the account holder or their legal heirs for a prolonged period. Such assets include:

*Bank deposits such as savings accounts, current accounts, fixed deposits, and recurring deposits that have not been operated for ten years or more.

*Insurance policy proceeds that remain unpaid beyond the due date

*Mutual fund redemption proceeds or dividends that could not be credited due to reasons such as a change in bank account, bank account closure, incomplete bank account in records, etc.

*Dividends and shares that remain unclaimed and are transferred to statutory authorities

*Pension and retirement benefits that are not claimed within the normal course

In most cases, assets may become unclaimed because of routine life events such as migration for work, changes in contact details, closure of old bank accounts, or lack of information among family members and legal heirs.

The Government is coordinating with the Reserve Bank of India (RBI), the Insurance Regulatory and Development Authority of India (IRDAI), the Securities and Exchange Board of India (SEBI), the Investor Education and Protection Fund Authority (IEPFA), and the Pension Fund Regulatory and Development Authority (PFRDA) to help citizens identify, access and reclaim financial assets that legally belong to them, using simple processes and transparent systems.

Business

Iran-Israel Conflict Hits India’s Real Estate: Supply Disruptions & Rising Costs Delay Project Possessions

Mumbai: The ongoing geopolitical tensions in West Asia, particularly the Iran–Israel conflict, have The ongoing geopolitical tensions in West Asia, particularly the Iran-Israel conflict, have begun to weigh on India’s real estate sector. Developers are flagging delays in project completion due to supply chain disruptions and rising input costs.

Industry stakeholders said shortages of key finishing materials such as tiles and sanitaryware, driven largely by gas supply constraints, are emerging as a critical concern. These disruptions are expected to push possession timelines, especially for projects in advanced stages.

CREDAI-MCHI Chief Operating Officer Keval Valambhia noted that the war has led to significant supply-side challenges. Shortages of gas and LPG have impacted the production of energy-intensive materials like supply of tiles from Morbi, which supplies over 80% of the market need. “Distributors have increased prices due to limited availability, but the situation remains manageable currently,” Valam bhia said. He warned that if the conflict continues, project possession timelines could extend by two to three months.

The marble and tile industry has been hit particularly hard. Gajendra Bhandari, President of the Vile Parle Marble Association, said that nearly 80% of factories have shut down. According to Bhandari, major firms are now insisting on full advance payments and have stopped accepting new orders without prior confirmation.

Deep Vadodaria, CEO of Nila Spaces, explained that the conflict affects projects at multiple levels. Beyond finishing materials like façade glass, core inputs like steel and cement are witnessing price pressure due to rising crude oil prices. Vadodaria described this as an indirect “wartax” on the sector, where developers deal with both cost escalations and procurement uncertainty.

Anand Gupta, a member of the Builders Association of India, said the availability of sanitaryware is hampered by chemical supply issues.

New Delhi, April 1: The Central Bureau of Investigation on Wednesday registered a case against Reliance Communications Ltd (RCom), Anil Ambani, unknown public servants, and unknown others on allegations of causing wrongful loss of Rs 3,750 crore to Life Insurance Corporation (LIC) of India.

The case has been registered on the basis of a complaint received from Life Insurance Corporation of India Ltd. for offences of conspiracy, cheating, misappropriation, and offences under the Prevention of Corruption Act, according to an official statement.

It is alleged that LIC was fraudulently induced to subscribe to Non Convertible Debentures (NCDs) worth Rs 4,500 crore on the basis of false representations made by Reliance Communications Ltd. and its management regarding the financial health of the company, and security and asset cover offered to LIC while subscribing to the NCDs.

The LIC has made this complaint on basis of a forensic audit report dated October 15, 2020 conducted by BDO India LLP, which reported that RCom and its management had resorted to misutilisation of funds raised from banks and financial institutions, routing of funds through subsidiaries, misuse of sale invoice financing, discounting of fictitious bills, systematic siphoning of funds through inter-company deposits and shell related entities, creating and write-off of fictitious debtors and receivables and gross overstatement of security. There was a mismatch between the charges and the assets.

Investigation of the case is in progress, the statement added.

The CBI had earlier registered three cases against RCom Ltd, Anil Ambani, and others on allegations of defrauding a number of banks.

Anil Ambani was also interrogated by the CBI at its head office in Delhi for two days in a row in connection with the alleged Rs 2,929.05 crore SBI fraud case.

The CBI had registered an FIR on August 21, 2025, following a complaint filed by the SBI, in which Reliance Communications Limited, Anil D. Ambani and others, including unknown public servants, are accused.

The State Bank of India (SBI) is the lead bank in the consortium of 11 banks — Bank of India, Central Bank of India, UCO Bank, Union Bank of India, e-Corporation Bank, Canara Bank, e-Syndicate Bank, Indian Overseas Bank, IDBI Bank Limited, and e-Oriental Bank of Commerce that had extended loans to the Anil Ambani group.

The complaint is based on a forensic audit report that alleges large-scale diversion and misutilisation of loan funds through interlinked and circuitous transactions among group entities during the period 2013-17, resulting in wrongful loss of Rs 2929.05 crore to the SBI out of total exposure of Rs 19, 694.33 crores involving 17 public sector banks, according to an official statement.

Subsequent to the registration of the case, separate complaints were received from the Punjab National Bank, the Bank of India, the Union Bank of India, the UCO Bank, the Central Bank of India, the IDBI Bank, and the Bank of Maharashtra. Further, another case has been registered against Reliance Communications Limited, Anil Ambani and others unknown, including unknown public servants, on February 25 on the basis of a complaint dated February 24, received from the Bank of Baroda, which includes exposure of e-Dena Bank and e-Vijaya Bank.

New Delhi, March 31: Gold loans have emerged as the leading segment in India’s retail credit market, accounting for loan volumes at 36 per cent and around 40 per cent by value, driven by rising gold prices and increasing consumer preference for secured borrowing, a report said on Tuesday.

The report by TransUnion CIBIL showed that the surge has been supported by a sharp increase in ticket sizes, with the average gold loan amount rising significantly over the past two years to around Rs 1.9 lakh in the December 2025 quarter.

The report also noted that the consumer market indicator (CMI) — a major gauge of credit market health — rose to 102 in the December 2025 quarter, up from 97 a year ago and 100 in the preceding September quarter which is the third consecutive quarter of improvement.

It further highlighted that gold prices have encouraged consumers to unlock value from their holdings, leading to a strong rise in both loan demand and disbursements.

Notably, gold loans are witnessing expansion beyond their traditional stronghold in southern India, with faster growth now seen in northern and western states such as Uttar Pradesh, Madhya Pradesh and Rajasthan.

The segment is also attracting a more diverse borrower base, with over half of the loans being availed by prime and above-category customers, indicating growing acceptance of gold loans as a mainstream credit product.

The report noted that while credit supply eased following festive demand and GST-related momentum, the moderation reflects seasonal trends rather than a structural slowdown.

Demand for credit remained strong, particularly in semi-urban and rural areas, with non-metro regions accounting for 54 per cent of the total borrower base, up three percentage points year-on-year. The share of new-to-credit consumers also increased to 15 per cent.

Meanwhile, auto loans saw stable volumes during the post-festive period, supported by demand in the affordable mid-segment category, while supply in the segment rose on a daily average basis compared to the previous year.

Additional Municipal Commissioner directs to resolve complaints of polluted water supply in Mumbai on immediate and priority basis

Mumbai Shivaji Nagar Two hammock raids: Case registered against fake doctor

50 gangsters arrested in Mumbai suburbs, police action against several gangsters in Zone 7, including Ghatkopar.

Mumbai : BMC continues to repair drains on a war scale before the rainy season, increasing the speed of rainwater

Padgha ISIS liaison Aqib Nachan arrested in other cases including timber and sandalwood smuggling, remanded till April 6

Married Mumbai Woman Mocked In Andheri Society Over ‘Lift Kissing’ CCTV Video, Files Police Complaint

LPG Crisis In Maharashtra: Cyber Crime On Rise Amid Shortage, 2 Women Lose ₹4 Lakh In ‘Gas Update’ Online Scam In Kalyan-Dombivli

Mahayoti’s big gift to the people of Mumbai… Now there is no tax for houses up to 500 square feet, the Municipal Corporation has increased this limit to 700 square feet.

Dhurandhar 2 Box Office Collection Day 1: Ranveer Singh Starrer Takes An Exceptional Opening; Crosses ₹100 Crore Mark

Govandi ISIS propaganda case: Ayan arrested… Anjuman-e-Islam Kalsekar College also on the radar, how did the second student come into contact with ISIS, investigation underway

-

Crime4 years ago

Crime4 years agoClass 10 student jumps to death in Jaipur

-

Maharashtra1 year ago

Maharashtra1 year agoMumbai Local Train Update: Central Railway’s New Timetable Comes Into Effect; Check Full List Of Revised Timings & Stations

-

Maharashtra1 year ago

Maharashtra1 year agoMumbai To Go Toll-Free Tonight! Maharashtra Govt Announces Complete Toll Waiver For Light Motor Vehicles At All 5 Entry Points Of City

-

Maharashtra2 years ago

Maharashtra2 years agoFalse photo of Imtiaz Jaleel’s rally, exposing the fooling conspiracy

-

National News1 year ago

National News1 year agoMinistry of Railways rolls out Special Drive 4.0 with focus on digitisation, cleanliness, inclusiveness and grievance redressal

-

Maharashtra1 year ago

Maharashtra1 year agoMaharashtra Elections 2024: Mumbai Metro & BEST Services Extended Till Midnight On Voting Day

-

National News2 years ago

National News2 years agoJ&K: 4 Jawans Killed, 28 Injured After Bus Carrying BSF Personnel For Poll Duty Falls Into Gorge In Budgam; Terrifying Visuals Surface

-

Crime1 year ago

Crime1 year agoBaba Siddique Murder: Mumbai Police Unable To Get Lawrence Bishnoi Custody Due To Home Ministry Order, Says Report